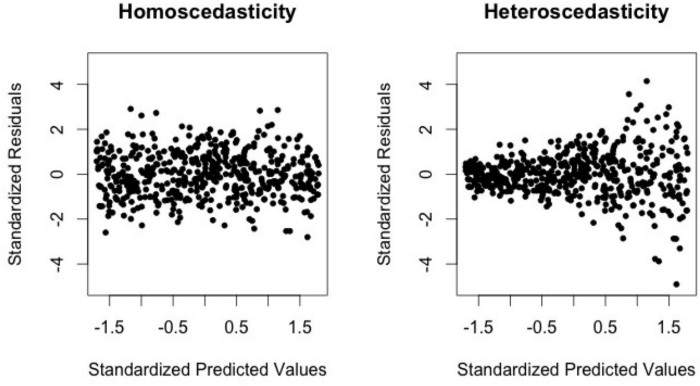

Heteroscedasticity is a condition where the error variance is not constant on the independent variable. Whereas Homoscedasticity is a condition where a variance error is constant in any condition of the independent variable.

The assumption of homoscedasticity is very important in terms of the linear regression model, the result of linear regression will become unreliable if this assumption is not fulfilled. Read more…